Amazon revenue has increased from just under $90B in 2014 to $638B in calendar 2024.

In 2014, AWS revenue was $4.6B, and this year (2025) it will likely end at a run rate near $130B. Operating income improved from $36.9B in 2023 to $68.6B in 2024, with operating margins increase from 6.4% to 10.8%.

Bezos famously ran Amazon to report zero operating profits on purpose. Why? Because if you don’t have profits then you don’t pay taxes. As long as you have attractive investments to make in the business paying taxes is a squandered opportunity.

These days I’m feeling a little bit like I’m in the twilight zone. Wall Street and the Xverse is abuzz with criticisms of the massive capital expenditures being laid out by Big Tech. Massive capex doesn’t just suck up cash today, it depresses earnings through depreciation into the future. It also increases operating expenses in perpetuity as more people are needed to manage the larger capital base. Still, shouldn’t we all be thrilled that these giant companies with stellar decades long track records believe they still have markets to go after that justify $80B annual capex budgets?

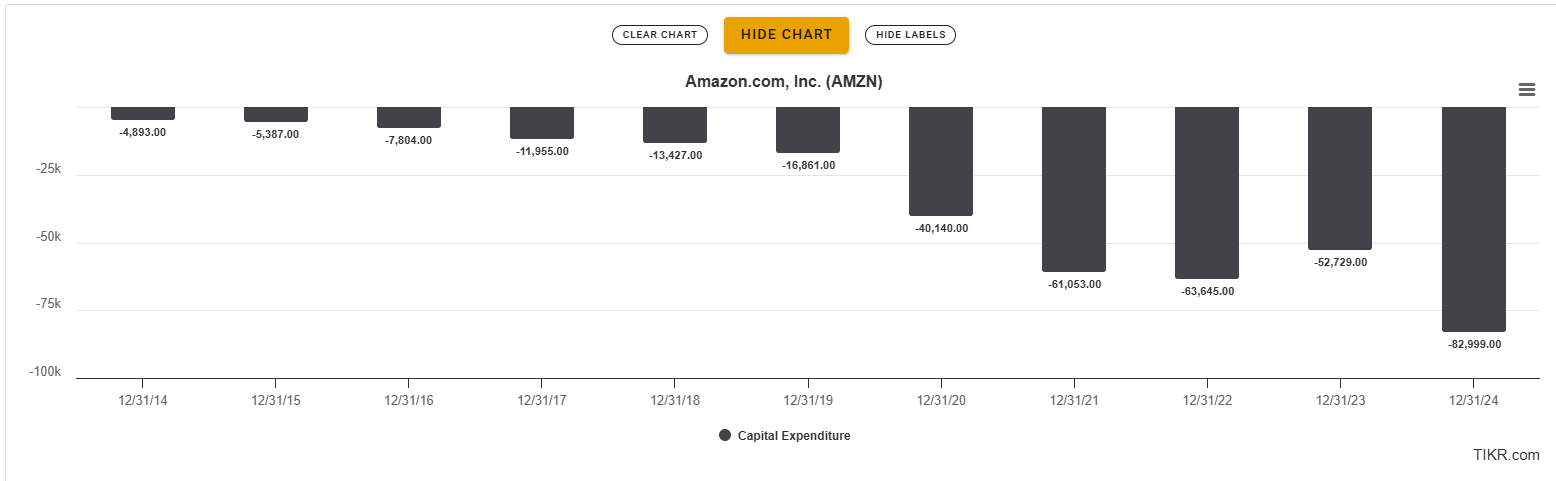

Amazon’s capex has increased from $4.9B in 2014 to $83B TTM and will likely be higher next year. This capex budget makes it possible to order products at night and get them delivered by morning in most big cities (by 2025 year’s end). It runs a substantial portion of the internet’s websites. The machines who are waking up are powered by it.

The only thing that worries me about Big Tech is that they are very obvious targets in a trade war. How easy would it be for Europe to just decide to charge them 5% of revenues generated on their turf? Or maybe 10%? Still, I don’t think such draconian measures would last long. I remain of the opinion that in the United States we live in a “Big Technocracy”. Despite Trump being the most powerful president of my 40 year lifetime - I do NOT think he is more powerful than the collection of tech companies who call America home.

Regarding Amazon specifically. If there is any single company ON EARTH that should be considered “anti-fragile” → that business is Amazon. I would feel more comfortable holding Amazon shares than any other through a zombie apocalypse. It’s business is extremely diversified. I put in my own figures for “True Margins” - which are simply what my best guess is they would average out to long term if Amazon made their objective maximizing operating margin - something they will never do as long as they are optimistic about growth opportunities.

Amazon - if it wanted - could have the most profitable advertising business on Earth. Their advertising business is defended by the 500 million + square feet of warehouse space. And a delivery infrastructure (I know you see the vans everywhere!) that is larger than anyone but the US Postal Service (and more advanced to boot).

The pandemic showed us that - in fact - ALL big tech companies are anti-fragile. But Amazon moreso than anyone. Over the course of just three years amazon DOUBLED the size of it’s fulfillment network. Having an ability to marshal and put to work that amount of resources is in itself an incredible skillset. Over the past twenty-four months Amazon has shown us that it can manage doubling capex from an already world-leading size at the same time as skyrocketing its operating margins.

Amazon describes itself as the “World’s most customer-centric company”. They are obviously deserved of this title. It’s easy to forget that Amazon essentially invented customer ratings, free no-questions asked returns, and reliable shipping. Before Amazon (I’m old enough to remember), if you ordered something on the internet or in a catalogue it would probably take “between 1 and 2 weeks” to arrive. If it didn’t arrive you would need to spend hours figuring out who to blame and chase for your money. And don’t you remember retailers being unwilling to accept returns if you lost the paper receipt?

Amazon turned their own experience selling retail products into Third Party Services - which I believe will someday be worth $1T.

It turned its own experience scaling digital infrastructure into AWS - which is arguably already worth $1T.

There is an enormous amount of optionality embedded in Amazon’s business. IF any company is going to crack healthcare in this country it is likely to be Amazon. Why not deliver medicine as a service to all prime members? Once autonomous vehicles are a thing why not make a Prime subscription option that comes with autonomous vehicles? Is anyone better positioned than Amazon to invest in automation and robotics? They employ some 1.5 million people - their payroll is now larger than any company on Earth except Walmart. That represents a lot of incentive to figure out how to automate. And what about satellites? Amazon wants to compete with SpaceX via their Kuiper business. Who else has a prayer? Why not include high speed internet with a Prime membership? My personal expectation is that SpaceX and Amazon will become an oligopoly that mops the floor with the big telecom companies. That’s a lot of revenue for the taking.

Below is an excerpt from Andy Jassy’s letter that speaks to optionality:

Fourth, speed disproportionately matters for every business, in every industry, at all times. It’s a false binary to argue that you can move fast or deliver high standards. If you want to be fast, you can be fast, and still be high quality. We’ve done it for many years (though we can still be faster). Speed is a leadership decision. The leadership team has to believe it’s a priority, reinforce it constantly, organize and remove structural barriers, and build in modular ways that enable pace. But, speed does not happen unless the entire company and culture embrace it. We have this persistent feeling, throughout the company and in every business in which we operate, that there are closing windows all around us. We operate in fiercely competitive market segments, with highly talented, well-funded, ambitious companies at every turn. Customers are always looking for something better. We spend a lot of time identifying how to unlock these experiences for them as quickly as possible, and know if we don’t, somebody else will.

This type of thinking is rare, particularly for large organizations. This type of thinking is completely extinct in Europe, Japan, and virtually everywhere except for the United States and China. Thinking like this is - literally - illegal in most parts of the world. How so? Because speed is impossible where labor laws are strict. Therefore - no one even practices the “mental muscle” of moving fast.

Economic chaos, the disruption caused by AI (e.g. to the jobs market), China taking an indominable lead in manufacturing scale AND prowess - there are many tectonic shifts underway that will destroy companies who are not nimble - but they will be extremely beneficial to companies who are. Amazon’s AI revenue is growing at over 100% Year on Year…

A few interesting tidbits to end on

-Amazon Prime started with unlimited, free, two-day delivery for 1 million products. It’s now grown to 300 million items and has 10s of millions available for same day delivery.

-Project Kuiper (the satellites) first target is the 400-500 million people around the world who don’t have access to broadband connectivity. Amazon expects the business to contribute meaningful operating income and be a high ROIC deployment.

-Lastly, this re-print from the 1997 letter by Bezos to shareholders showing just how far Amazon has come. 285,000 square feet of warehouse space in 1997 has turned into 500 million and growing!

VC Bill Gurley calls Jeff Bezos "the best entrepreneur that I've ever been around or got to know".

He institutionalized a culture of experimentation and risk seeking at Amazon that doesn't exist at any other large company.

https://www.youtube.com/watch?v=TVfjS_l16mQ

That's why Amazon is so anti-fragile and can compete vigorously on so many fronts.

Not for Everyone. But maybe for you and your patrons?

Dear Ben,

I hope this finds you in a rare pocket of stillness.

We hold deep respect for what you've built here—and for how.

We’ve just opened the door to something we’ve been quietly handcrafting for years.

Not for mass markets. Not for scale. But for memory and reflection.

Not designed to perform. Designed to endure.

It’s called The Silent Treasury.

A sanctuary where truth, judgment, and consciousness are kept like firewood—dry, sacred, and meant for long winters.

Where trust, vision, patience, and stewardship are treated as capital—more rare, perhaps, than liquidity itself.

The two inaugural pieces speak to a quiet truth we've long engaged with:

1. Why we quietly crave for signal from rare, niche sanctuaries—especially when judgment must be clear.

2. Why many modern investment ecosystems (PE, VC, Hedge, ALT, SPAC, rollups) fracture before they root.

These are not short, nor designed for virality.

They are multi-sensory, slow experiences—built to last.

If this speaks to something you've always felt but rarely seen expressed,

perhaps these works belong in your world.

Both publication links are enclosed, should you choose to enter.

https://tinyurl.com/The-Silent-Treasury-1

https://tinyurl.com/The-Silent-Treasury-2

Warmly,

The Silent Treasury

Sanctuary for strategy, judgment, and elevated consciousness.